This is the summary of a paper issued as Working Paper no. 12-2021, Department of Economics, Athens University of Economics and Business. Earlier versions of this paper were presented in seminars at the Athens University of Economics and Business (2014), Boston College (2017) and the ASSET Conference in September 2019.

The paper has been published in the June 2021 issue of the Journal of Economic Asymmetries.

_____________________________________________

The area of international trade and international finance is replete with paradoxes. While our basic models and theories suggest that free international trade, labor migration and capital mobility should result in higher welfare, trade protectionism, migration restrictions, capital controls and sovereign debt crises are still more prevalent than what would be justified by our theories.

In the area of international finance, two of the major paradoxes are the Feldstein Horioka (1980) ‘puzzle’, of the high correlation between domestic savings and investment rates and the Lucas (1990) ‘paradox’ of the low capital flows from capital rich to capital poor economies. These two paradoxes suggest that even after international financial liberalisation world capital markets fail to function as predicted by our basic theoretical models. For other major paradoxes in international macroeconomics see Obstfeld and Rogoff (2000).

In addition, the frequency of international debt crises in the era of financial openness since the liberalization of international capital markets in the 1970s, such as the Latin American, Asian and Euro Area crises, suggests that such markets are characterized time consistency problems which frequently undermine financial openness and the concomitant benefits of inter-temporal trade. For the historical evidence on debt crises see Reinhart and Rogoff (2009). For a recent empirical analysis of the relation between debt and financial crises see Kose et al (2020).

One recent case in point is the experience of the economies in the periphery of the euro area (Greece, Portugal, Spain and Ireland), analysed by the contributors in Baldwin and Giavazzi (2015). These economies opted for full financial openness when they entered the euro area at the end of the 1990s. Their adoption of the euro was interpreted as a non-default clause. As a result, for almost ten years they experienced low real interest rates, high investment and growth rates and lower national savings rates. Their current account deficits soared and they were the first to be hit in the international financial crisis of 2008. They subsequently returned to high real interest rates and some were excluded from international financial markets. Had it not been for conditional official lending from other countries of the EU and the IMF, they would have effectively returned to a regime of financial autarky.

In a recent paper, Alogoskoufis (2021), I have examined and tried to explain both of these paradoxes in the context of a two country extended version of the Ramsey (1928) model of optimal growth. The use of this standard neoclassical model in international macro-economics has been relatively limited, due to the assumption of the canonical version of the model that investment is determined by domestic savings.

The paper uses a version of the Ramsey model augmented by the q-theory of investment, which allows for the decoupling of the savings behaviour of households from the investment decisions of firms. While in the canonical open economy version of the optimal growth model the optimal level of foreign borrowing is achieved instantly, and there is no convergence process or current account dynamics, this is not the case in the augmented model. For a small open economy version of the augmented Ramsey model see Blanchard and Fischer (1989).

The analysis is based on the distinction between two types of economies, a ‘poor’ and a ‘rich’ economy. A ‘poor’ economy is defined as an economy with a ‘low’ initial capital stock, relative to its balanced growth path, and a ‘rich’ economy as an economy with a relatively ‘high’ initial capital stock. All the other parameters are assumed to be the same for both economies. Thus, for a ‘poor’ economy, the initial equilibrium real interest rate under autarky is higher than the initial world real interest rate that it faces under financial openness and the opposite applies for a ‘rich’ economy.

For both types of economy, there are welfare gains from financial openness as long as there is pre-commitment on the part of international borrowers not to default. In such a case, financial openness affords both types of countries opportunities for welfare enhancing inter-temporal trade. A poor economy can increase welfare by trading higher consumption during the initial period of convergence towards the steady state, for lower consumption in the latter period and the steady state itself. A rich economy can increase welfare by trading higher savings during the initial period of the convergence process, for higher consumption in the steady state. This inter-temporal trade takes place through adjustments in the trade balance and the current account.

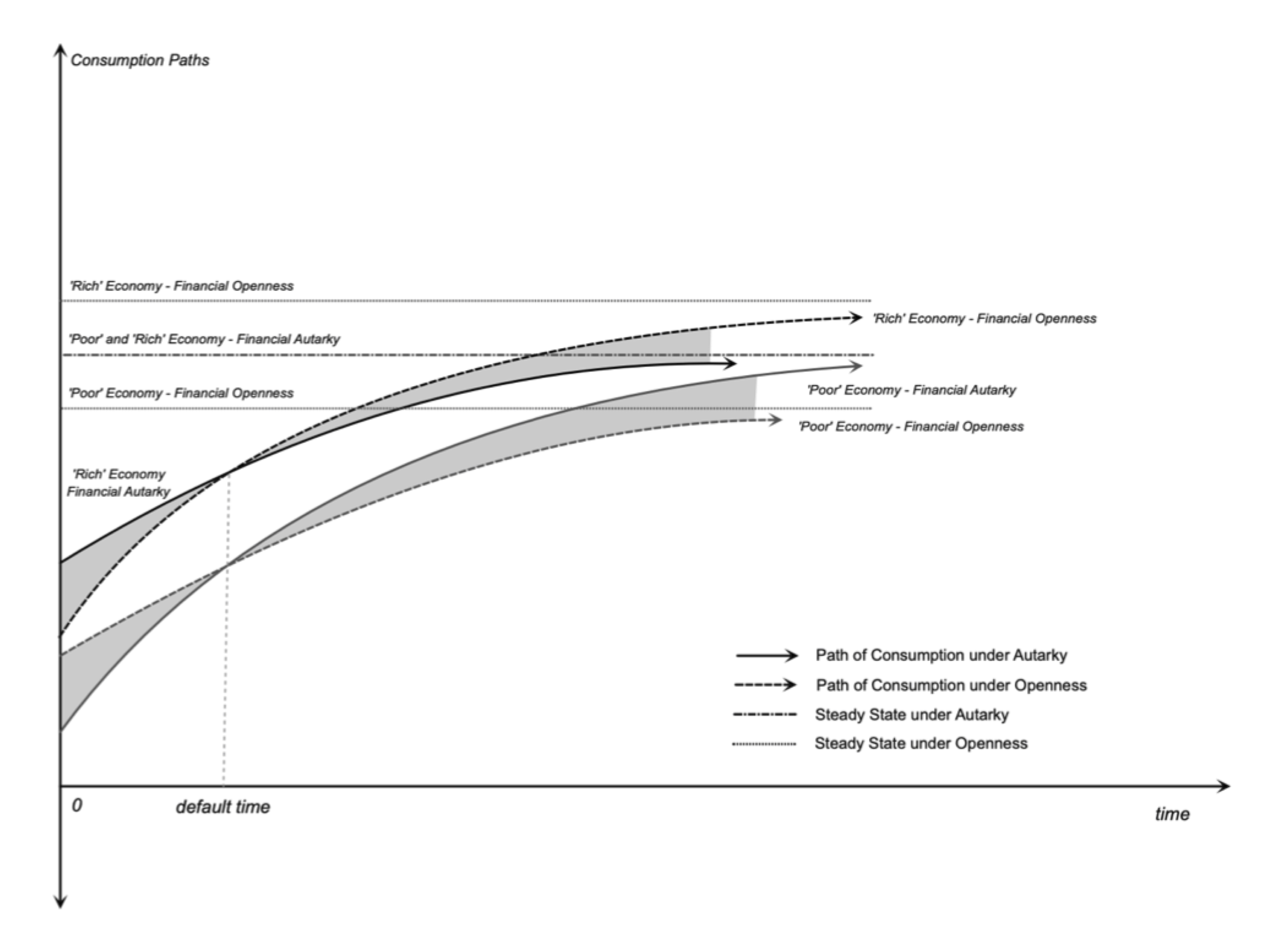

The dynamic paths of consumption for the two economies, under financial autarky and financial openness are depicted in Figure 1.

Under financial autarky, the consumption path of the poor economy implies lower consumption (per efficiency unit of labor) than the rich economy, but over time, they both approach the same steady state level of consumption (and output), as they are assumed to share the same preference and technology parameters.

Financial openness allows consumers in the poor economy to borrow at the world interest rate which lies below its own ‘autarky’ real interest rate and the ‘autarky’ real interest rate of the rich economy. Hence, initially, the consumption path of the poor economy lies above its ‘autarky’ consumption path, while the opposite happens for the rich economy which under financial openness becomes an international lender. For some time, the poor country runs current account and trade deficits, because of its higher consumption level relative to financial autarky and the opposite happens for the rich economy. This process is subsequently reversed.

Comparing financial openness under pre-commitment with financial autarky, one reaches the following conclusions from the analysis of the model:

- On the balanced growth path, gross domestic product (GDP) per capita under financial openness is the same as under autarky for both economies. This is because their only difference is assumed to lie in their initial capital stock.

- Gross national income (GNI) and consumption per capita under financial openness are lower than in the case of financial autarky for the poor economy, since it has to pay interest on the foreign debt it has accumulated during the transition. The opposite applies to the rich economy.

- During the transition, the rich economy runs current account surpluses and accumulates net foreign assets, while the poor economy runs current account deficits and accumulates net foreign debt.

- The balanced growth path is characterized by external balance, in the sense of constant net foreign assets (per effective unit of labor), for both the rich and the poor economy. The rich economy is a net international creditor, and the poor economy is a net international debtor.

- There are benefits from inter-temporal trade for both types of economies. However, a dynamic numerical simulation of the model suggests that the present value of these benefits is extremely small, of the order of only 0.33%. This finding is consistent with Gourinchas and Jeanne (2006) who used a standard growth model without current account dynamics.

- The benefits of financial openness are “front loaded” for the poor economy and the costs are “back loaded”. The opposite is the case for the rich economy. Both consumption and investment rise initially relative to autarky in the poor economy, resulting in a period of trade deficits and high welfare benefits, which has to be followed by a period of trade surpluses and a gradual reversal of most of the initial welfare benefits. The opposite happens in the rich economy.

Because of the accumulation of international debt, there is a sharp intertemporal tradeoff. A numerical simulation of the model suggests that after the first 30 years (periods) of the adjustment, for which the poor economy is running trade deficits, the discounted utility of the representative household under financial openness is 14.2% higher than under financial autarky. However, most of these benefits evaporate in the remainder of the transition, as the poor economy has to run subsequent trade surpluses in order to cover the interest payments on its accumulated foreign debt. Consumption thus eventually settles below the autarky level. On the other hand, the rich country faces the opposite tradeoff. It optimally trades lower early consumption for higher future consumption, including higher steady state consumption than under financial autarky. The reason is that as a net creditor, it receives additional interest income on its positive steady state net foreign assets.

This asymmetric intertemporal tradeoff creates incentives for the poor economy to default. The optimal path is time inconsistent in the sense of Kydland and Prescott (1977). The incentive arises at the instant when the path of the consumption of the poor country under financial openness crosses the corresponding path under financial autarky from above (Figure 1). By defaulting on its foreign debt at this point, the poor country can achieve a higher future consumption path under autarky, including higher steady consumption. Default increases future welfare. Thus, in the absence of effective pre-commitment mechanisms that preclude default, or effective sanctions, the poor economy will certainly default.

In the absence of precommitment, the eventual default will be anticipated by international lenders (the rich economy), which will not lend to the poor economy at the world real interest rate, but only at the autarky interest rate of the poor economy. Hence, financial openness will break down and, in the absence of pre-commitment, financial autarky will prevail even if there are no legal restrictions to financial openness. Domestic savings will be equal to domestic investment for both poor and rich economies, accounting for the Feldstein-Horioka ‘puzzle’, and capital will not flow from the rich to the poor country, accounting for the Lucas ‘paradox’.

Official lending through international institutions like the IMF, the World Bank and other international development banks, sanctions in the case of default, and strong pre-commitment mechanisms may help break the deadlock. The paper briefly discusses such mechanisms starting with pre-commitment mechanisms.

Pre-commitment mechanisms can take a direct form, such as binding constitutional restrictions on nationalizations of foreign assets or default of foreign debt, binding clauses in international debt contracts that refer disputes to the jurisdiction of courts in the lender country, or the signing of binding international treaties or loan agreements with international economic organizations to which debtor nations belong, such as the World Bank, the IMF or the OECD. Such agreements could imply pre-commitment not to default, conditionality and continuous monitoring. Pre-commitment mechanisms can also take an indirect form, through participation in a broader economic area, such as a free trade area, a customs union, or a single market, like the European Union, with rules that effectively preclude sovereign defaults. Yet, as the frequency of sovereign debt crises suggests, these pre-commitment mechanisms have not proven to be particularly effective.

The paper also analyses sanctions as full or limited solutions to the time inconsistency problem. Sanctions can indeed take many forms. From the “gunboat” diplomacy of the 19th century, to the trade and other economic sanctions of the 20th and 21st century.

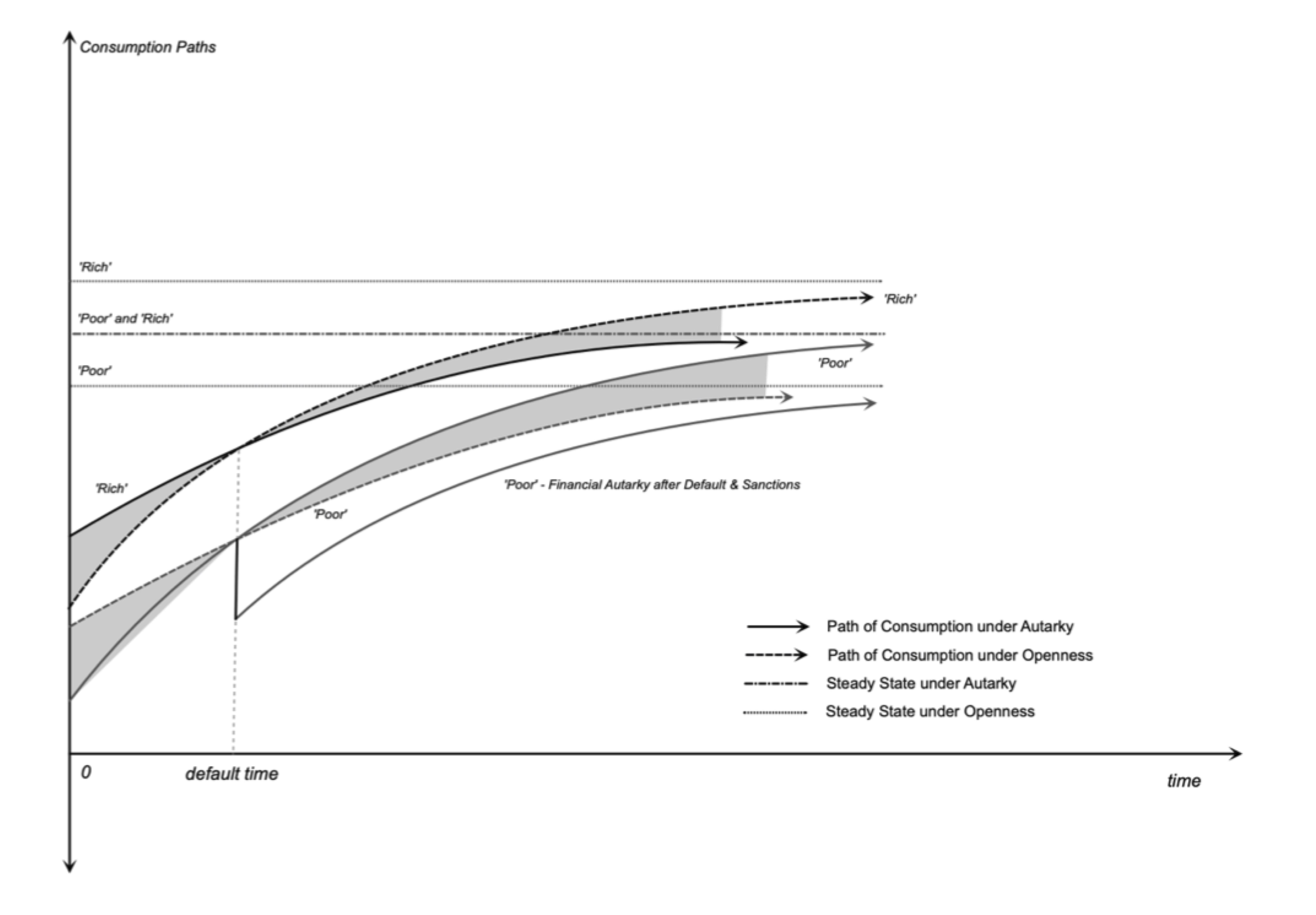

The effects of sanctions can be gleaned from Figure 2. If international creditors could impose permanent sanctions in the case of default, with an instantaneous cost equal to or greater that the difference between the autarky and openness consumption level of the poor country, then the incentive to default would never arise. As soon as the poor country defaulted it would return to financial autarky, but would also have to pay the additional cost implied by the sanctions. If this cost was greater than or equal to the benefit of default, then default would never arise. The poor economy would continue servicing its foreign debt in order to avoid the sanctions.

However, effective sanctions, may be quite large and infeasible. For example, in the case of our simulations of the model, for the sanctions to be effective they must amount to a per period cost of between 2-5% of the debtor nation’s GDP, with a present value of between two (2) and five (5) times a nation’s GDP. What if sanctions of this magnitude are not feasible? Then the threat of imposing effective sanctions would not be credible. Lower sanctions would work, but only in conjunction with capital market restrictions. One such restriction is a foreign debt ceiling. A debtor country would never default if the maximum amount it was allowed to raise in international capital markets implied a debt servicing cost lower than the cost of credible sanctions.

Conclusions from the analysis of time inconsistency can thus be summarised as follows:

- The ex ante optimal borrowing path of a poor nation is time inconsistent. Once the benefits of financial openness have been reaped, the optimal response involves defaulting on the already accumulated foreign debt and returning to financial autarky.

- The incentives of international borrowers to default will be anticipated by international lenders, who will not lend to poor nations, even if there are no legal restrictions to international borrowing and lending. In the absence of a solution to the time inconsistency problem of international borrowers, financial autarky is the only time consistent equilibrium. In such a case, capital would not flow from rich to poor countries, and the Feldstein Horioka ‘puzzle’ and the Lucas ‘paradox’ are fully explained.

- Full solutions to the time inconsistency problem of international borrowers require devising effective pre-commitment mechanisms that preclude default, or sufficiently large sanctions, the threat of which would stop a poor nation from defaulting and restore financial openness.

- If sufficiently large sanctions are not feasible, limited sanctions combined with foreign debt ceilings provide a partial solution to the time inconsistency problem. Capital would flow from rich to poor countries, but up to a foreign debt ceiling determined by the maximum feasible severity of sanctions.

References

Alogoskoufis, G. (2021), Asymmetries of Financial Openness in an Optimal Growth Model, Working Paper no. 12-2021, Department of Economics, Athens University of Economics and Business (published in the Journal of Economic Asymmetries, June 2021).

Baldwin, R. and Giavazzi, F. (2015), (eds), The Eurozone Crisis: A Consensus View of the Causes and a Few Possible Remedies, CEPR and VoxEU.org , London.

Blanchard, O.J. and Fischer, S. (1989), Lectures on Macroeconomics, Cambridge, MA., MIT Press.

Feldstein M. and Horioka C. (1990), “Domestic Saving and International Capital Flows”, The Economic Journal, 90 (358), pp. 314-329.

Gourinchas P.O. and Jeanne O. (2006), “The Elusive Gains from International Financial Integration”, Review of Economic Studies, 73 (3), pp. 715-741.

Kose, M.A., Nagle, P., Ohnsorge, F. and Sugawara, N. (2020), “Debt and Financial Crises: Will History Repeat Itself?”, VoxEU.org , 16 March 2020.

Kydland, F.E., and Prescott, E.C., (1977). “Rules rather than Discretion: The Inconsistency of Optimal Plans”, Journal of Political Economy, 85 (3), pp. 473-492.

Lucas R.E. Jr (1990), “Why Doesn’t Capital Flow from Rich to Poor Countries”, American Economic Review, Papers and Proceedings, 80 (2), pp. 92-96.

Obstfeld, M. and Rogoff, K. (2000), “The Six Major Paradoxes in International Macroeconomics: Is There a Common Cause?”, NBER Macroeconomics Annual, 15, pp. 339-390.

Ramsey F. (1928), “A Mathematical Theory of Saving”, The Economic Journal, 38 (152), pp. 543-559.

Reinhart, C.M. and Rogoff, K.S. (2009), This Time is Different: Eight Centuries of Financial Folly, Princeton, N.J., Princeton University Press.

___________________________