George Alogoskoufis

Working Paper no. 05-2026, Department of Economics, Athens University of Economics and Business

This study offers an analysis of the evolution of the international monetary system since the early nineteenth century, centered on a fundamental question: why has the United States dollar succeeded in achieving—and maintaining—global monetary dominance for such a long period of time?

It examines the transition from international bimetallism to the classical gold standard, the failed interwar attempt to restore monetary order through the gold-exchange standard, and the creation of the dollar-based Bretton Woods system after the Second World War.

The study then analyzes the operation and eventual collapse of the Bretton Woods system, the complete elimination of gold’s monetary role, and the transition to floating and managed exchange rates in the early 1970s—developments that, paradoxically, further reinforced the central role of the dollar in the global economy.

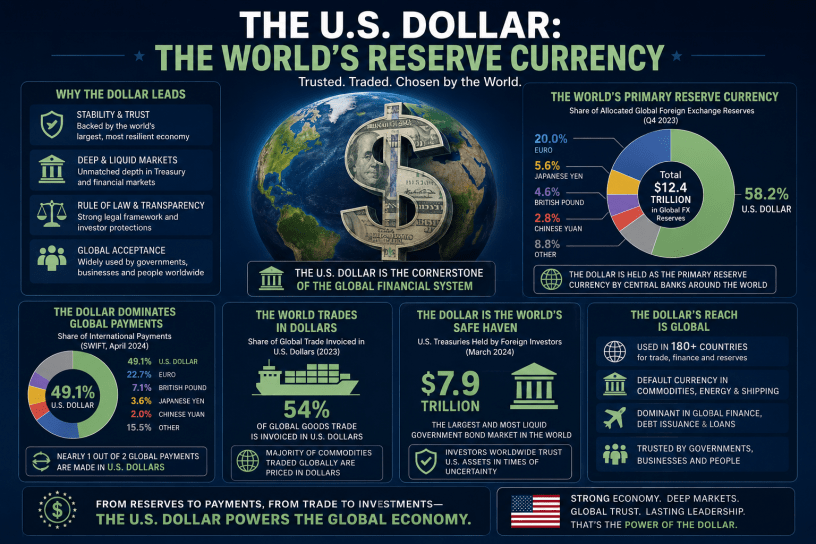

Today, the dollar accounts for approximately half of global payments, while more than half of world trade is invoiced in dollars. Close to 60 percent of international foreign exchange reserves are held in dollars. The corresponding share for the euro is about one fifth (20 percent), while other international currencies such as the Japanese yen, the pound sterling, and the Chinese renminbi each account for only low single-digit percentages. U.S. government securities held by international investors amount to $7.9 trillion, equivalent to nearly 10 percent of world GDP.

The dollar maintains its leadership because it is supported by the world’s largest and most resilient economy, rests on deep and highly liquid financial markets and a transparent rule-of-law framework, enjoys strong monetary credibility, and benefits from powerful network externalities as the most widely used international currency.

Looking ahead, the study evaluates the rise of the euro and the renminbi as potential challengers to the dollar, examining their institutional foundations, structural constraints, and global implications.

Combining historical narrative with rigorous economic analysis, this study argues that, despite the increasing multipolarity of the world economy, unless a global disruption of historic proportions occurs, the dollar’s position as the dominant international reserve currency is unlikely to be seriously challenged in the foreseeable future.