George Alogoskoufis

A short version of this article was published in Greek in the newspaper TA NEA, 9 May 2026

___________________________________________________________________________

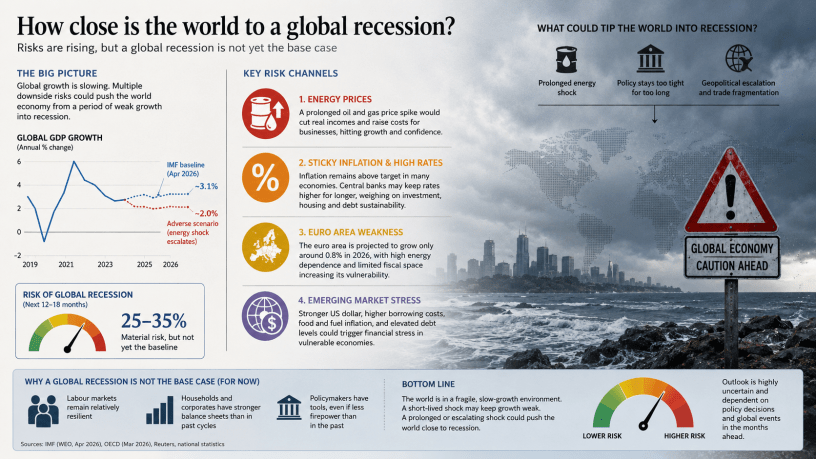

The world economy is once again flirting with an old and unwelcome question: not whether growth is slowing, but whether the slowdown will turn into a full blown recession. After a period of surprising resilience in the face of pandemic aftershocks, supply disruptions and war, the global expansion is losing momentum. Yet a full-blown global recession remains, for now, a risk rather than the baseline scenario. The uncertainty lies in the interaction of several powerful forces—energy prices, inflation, monetary policy and geopolitical tensions—whose combined effects are difficult to calibrate but increasingly hard to ignore.

At first glance, the outlook appears tolerable. Growth in the United States has proved sturdier than many expected, supported by robust labour markets and household balance sheets. In Asia, China’s economy, though structurally challenged, continues to expand, while India and parts of South-East Asia are benefiting from investment flows linked to supply-chain diversification. On current projections, global output is still expected to grow at a rate above the threshold commonly associated with recession.

Look beneath the surface, however, and the picture darkens. The most immediate risk stems from energy markets. Renewed tensions in the Persian Gulf have revived the spectre of a sustained rise in oil and gas prices. Such a shock would act as a tax on consumers and a cost burden on firms, squeezing real incomes and profit margins simultaneously. Unlike the disinflationary forces of the past decade, energy shocks are blunt and regressive, hitting poorer households hardest and constraining discretionary spending. For energy-importing regions, notably Europe, the effects are particularly acute.

The second concern is the persistence of inflation. Although headline inflation has receded from its peaks, core measures remain stubbornly elevated in several major economies. This stickiness reflects not only lingering supply constraints but also the strength of services demand and, in some cases, wage pressures. In addition, the rise in energy prices will cause inflation to rise, even temporarily. Central banks therefore find themselves in an awkward position. Having tightened policy aggressively to contain inflation, they are reluctant to ease prematurely for fear of reigniting price pressures. The result is a high interest-rate environment, which gradually tightens financial conditions and weighs on investment, housing markets and credit growth.

Nowhere are these dynamics more visible than in the euro area. Europe combines several vulnerabilities: weak underlying growth, a heavy dependence on imported energy and limited fiscal space in many member states. Industrial output in key economies has struggled to regain momentum, and consumer confidence remains subdued. Even modest external shocks can therefore tip the region into recession. In such circumstances, the euro area risks becoming the epicentre of any broader global slowdown, transmitting weakness through trade and financial channels.

Emerging markets face a different, but no less serious, set of risks. Higher global interest rates, particularly in the United States, have strengthened the dollar and increased the cost of servicing external debt. For countries with large financing needs, this creates a precarious balance. At the same time, elevated food and energy prices strain current accounts and exacerbate social pressures. While many emerging economies have improved their policy frameworks since past crises, the margin for error remains thin. A combination of tighter financial conditions and external shocks could still trigger episodes of instability.

Yet it would be premature to declare that a global recession is imminent. The global economy retains several sources of resilience. Labour markets in advanced economies, though softening, have not deteriorated sharply. Corporate balance sheets, in aggregate, are healthier than in previous cycles. And the financial system, while not immune to stress, is better capitalised than it was before the global financial crisis. Moreover, policymakers are not without tools. Should growth falter more sharply, central banks could eventually pivot, and governments could deploy targeted fiscal measures, albeit within tighter constraints than in the past.

The more plausible near-term scenario is therefore one of continued, uneven expansion—what might be described as a ‘slow-growth path’. In this environment, global output grows, but at a pace insufficient to generate strong income gains or to absorb shocks easily. Such a trajectory is inherently fragile. It leaves the economy exposed to tipping points, where an additional disturbance—be it an escalation in geopolitical tensions, a financial accident or a sharper-than-expected tightening of credit—could push growth into negative territory.

The history of global recessions offers a cautionary lesson. They rarely arise from a single cause. Rather, they emerge from the confluence of multiple vulnerabilities that reinforce one another. Today, many of those ingredients are present: geopolitical uncertainty, elevated debt levels, restrictive monetary policy and structural shifts in the global economy, from deglobalisation pressures to demographic change. What is missing, so far, is the catalyst that brings them together.

Whether such a catalyst will materialise depends largely on the evolution of the risks now in play. A stabilisation of energy markets, combined with a gradual easing of inflation, would allow central banks to reduce interest rates and support demand. Under such conditions, the global economy could muddle through. Conversely, a prolonged energy shock, coupled with persistently high inflation, would trap policymakers in a difficult bind and increase the likelihood of policy errors. In that scenario, the descent from slowdown to recession could be swift.

For now, the world economy stands at an uncomfortable juncture. It is not in recession, but neither is it securely on a path of sustained growth. The risks of a global recession are real and rising, even if they are not yet dominant. As so often in economics, the outcome will depend less on any single variable than on the interaction of many. That is what makes the current moment both manageable and dangerous: manageable, because there is still time to respond; dangerous, because the margin for error is narrowing.

© George Alogoskoufis

{kind=link}