from the European Commission, European Economy, May 2021

The COVID-19 pandemic, and the necessary containment measures to save lives following its outbreak, pushed Greece’s economy into a deep recession in 2020. Tourism and more generally, the services sector were particularly hit. Nonetheless, the timely policy measures taken by the Greek government have managed to cushion the downturn by supporting employment and business liquidity. Accommodative fiscal policy, coupled with the strong stimulus from the Recovery and Resilience Plan, are expected to help kick-start the economy going forward.

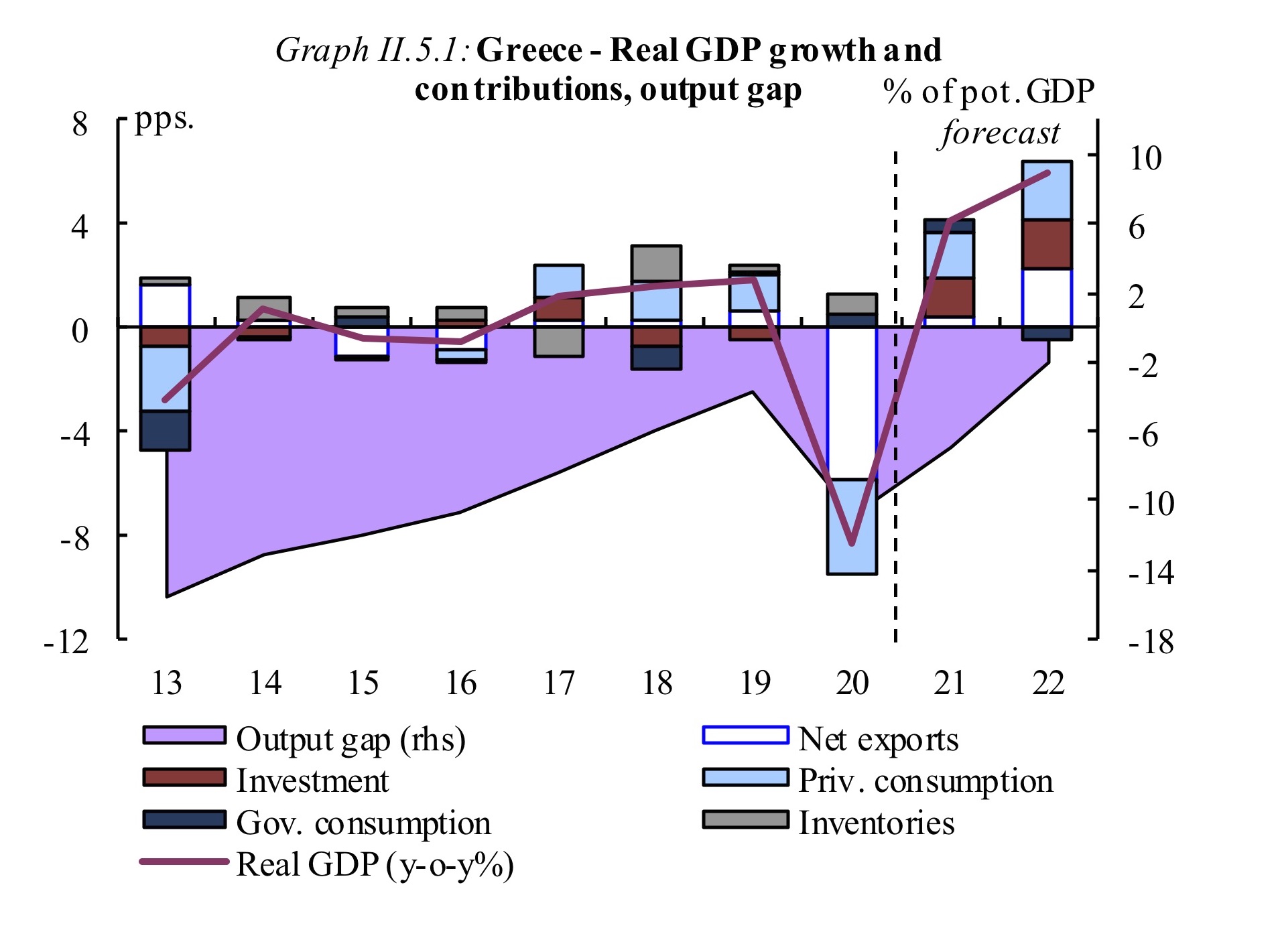

A significant contraction in 2020

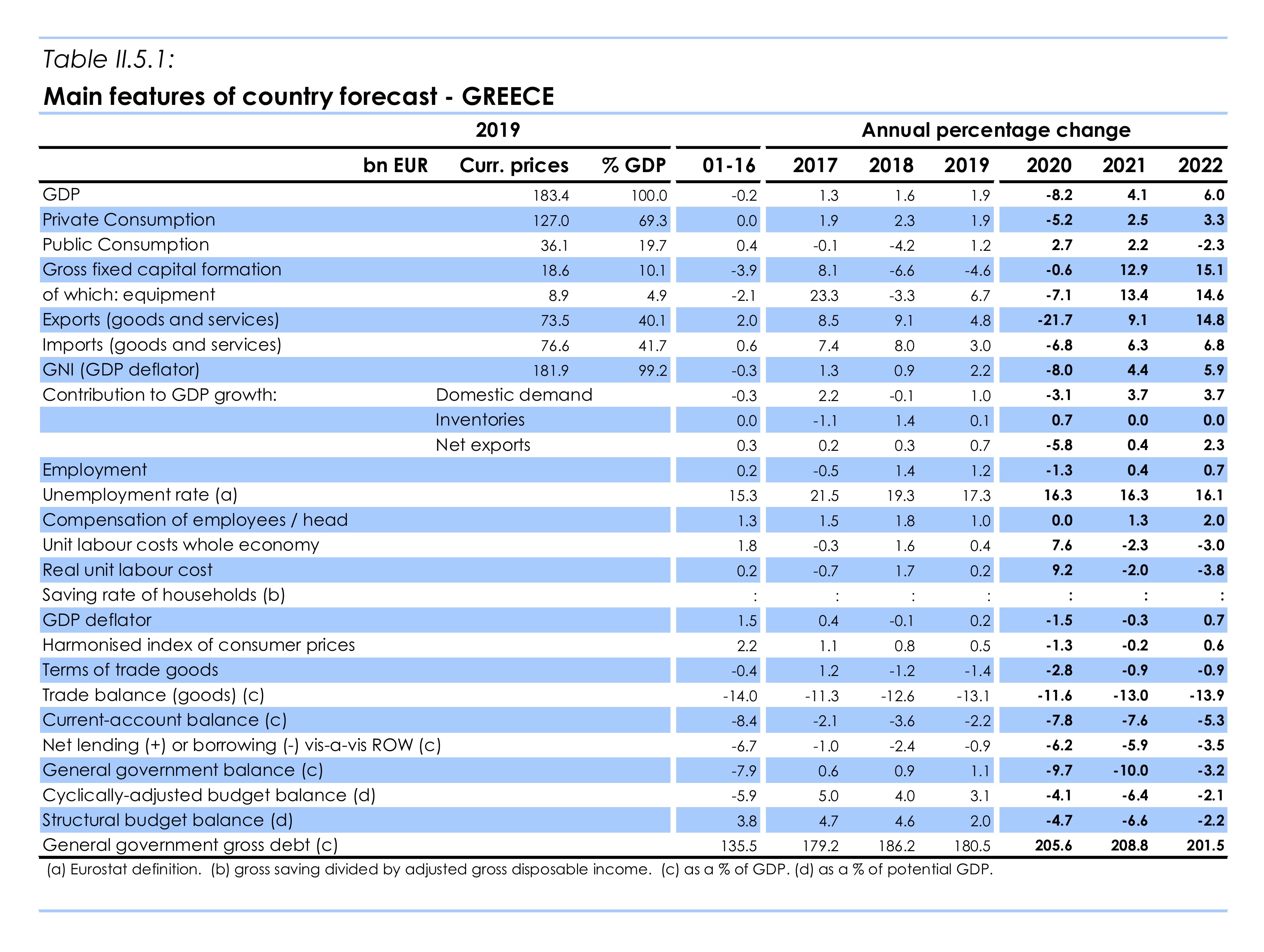

Greece’s economy contracted by 8.2% in 2020 due to the impact of COVID-19 pandemic and the containment measures taken in an effort to curb infections, especially during the second and fourth quarters of last year. The economic impact of the pandemic on Greece was substantial, particularly due to the importance of the tourism sector and the small size of the majority of enterprises in the economy. The impact on total investment, however, was relatively small, thanks to a timely increase in public investments and strong construction activity, which operated with limited restrictions during the lockdown periods. Employment support measures managed to prevent large-scale dismissals, keeping the unemployment rate at 16.3%, while employment decreased due to lower hiring in the tourism sector.

Investments under the Recovery and Resilience Plan: the backbone of the recovery

The ongoing rollout of the vaccination campaign should allow for a gradual easing of the containment measures, which were still in place in the first quarter of 2021. This should enable the realisation of purchases deferred from the previous year and contribute to private consumption growth, especially in 2022, where households should also benefit from the savings that have accumulated during the pandemic. Economic activity in the second half of this year is also expected to be supported by the launch of the implementation of the projects presented in Greece’s Recovery and Resilience Plan. Overall, GDP is forecast to grow by 4.1% in 2021 and 6.0% in 2022.

The gradual reopening of the tourism sector should support net exports, along with the projected market share gains for Greek exports, a trend that has been interrupted by the pandemic.

This forecast assumes that the impact of the pandemic on liquidity and incomes will continue to be cushioned by policy support. In particular, job support measures are expected to continue facilitating the return of workers, whose labour contracts have been suspended, to regular employment and help maintain the unemployment rate at 16.3% in 2021, unchanged from 2020. Job creation, however, is forecast to recover more slowly, and only support a reduction in unemployment in 2022, to 16.1%. Despite the recent hike in energy prices, overall inflation is likely to remain mildly negative in 2021, largely on account of weak demand for industrial goods and services, before gradually recovering in 2022.

Uncertainty remains high, particularly in relation to the tourism sector and the easing of travel restrictions. Additional risks come from the impact of the crisis on the solvency of firms that could arise once support measures end. Labour market developments will crucially depend on the pace at which labour support measures are phased out. External geopolitical factors remain a source of uncertainty.

Fiscal policy will support recovery

The deficit in Greece’s headline balance reached 9.7% of GDP in 2020, which can be mainly attributed to the cost of the measures adopted to mitigate the social and economic impact of the crisis (6.3% of GDP) and the impact of the pandemic on state revenues. In addition, the change in the statistical recording of the expected cost of clearing the backlog of state guarantees and the healthcare claw-backs resulted in an increased deficit in 2020.

The deficit in the general government balance in 2021 is expected to remain large (10.0% of GDP). Apart from the cost of the prolongation of the support measures adopted in 2020, the forecast takes into account new measures adopted to support the recovery, most importantly a reduction of social security contributions and the temporary abolition of the social solidarity tax for the private sector. The forecast also factors in a reduction of the rate of advance payments for the corporate income tax and a reduction of the tax itself by 2pps for profits made in 2021 and the following years.

As the economy continues to recover and emergency fiscal measures are gradually phased out, the headline deficit is expected to decline to 3.2% of GDP in 2022. As regards the Recovery and Resilience Plan, in the absence of sufficiently detailed information, this forecast assumes a simplified and linear integration of RRF-financed expenditure.

Fiscal risks remain substantial. They are related to state guarantees that were issued as part of the emergency measures in 2020 and could be called in the future. Additional risks might derive from the set-up of the planned sale and lease-back scheme for properties owned by vulnerable debtors, in case it is considered to be part of the general government. There are also risks stemming from litigation cases against the Public Real Estate Company (ETAD) and the ongoing legal challenges against earlier reforms.

Following a steep increase in 2020 linked to the pandemic, public debt is expected to slightly increase to around 209% of GDP in 2021 before declining to around 202% in 2022.