George Alogoskoufis

Historically, the two recurring major macroeconomic imbalances of the Greek economy are related to public finances and the balance of payments. Both the fiscal balance and the current account balance have been persistently negative, and have constituted the large twin deficits of the Greek economy. The twin deficits have resulted in growth pauses, long periods of monetary instability, excessive foreign borrowing, and periods of external debt crises and defaults.

Fiscal and monetary instability in the history of modern Greece was mainly the result of either the pursuit of the Great Idea, as in the last part of the 19th century and the first fifth of the 20th century, or the pursuit of the redistribution of income and wealth through public borrowing, as during and after the 1980s.

In addition, due to the insufficiency of national savings in relation to investment and tax revenues in relation to public expenditures, throughout the history of modern Greece, with the partial exception of the 1950s and 1960s, periods associated with easy access to international borrowing led to excessive external borrowing and debt and, ultimately, external debt crises and / or defaults.

One of their key features of emerging economies is that domestic savings are often insufficient to finance domestic investment opportunities. Emerging economies, like many developed ones, resort to borrowing from the international money and capital markets whenever they can, in order to finance the investment required and to promote their economic growth. However, unlike large developed industrial economies, the international debt of small emerging economies is usually in foreign currency and not in their own currency. This has happened in the case of Greece as well, throughout its history of the last 200 years.

High external borrowing in foreign currency makes an economy vulnerable if conditions or even expectations in the international financial markets change. If international investors start to believe that a country may not be able to continue servicing its foreign debt and that it may default, they will stop financing it, which causes a foreign debt crisis, even if the country is in fact solvent. Foreign currency loans or expiring foreign currency bonds are not renewed or, if renewed, international investors demand higher returns, causing debt service costs in foreign currency to rise. This can lead to an external debt crisis or even a default. In a developed economy that borrows in its own currency, this is not the case, because it always has the option to issue domestic currency to repay its debts.

Conditions for an External Debt Crisis or Default

There are four necessary conditions for a sovereign debt crisis or default:

First, high international liquidity and mobility of capital worldwide, which allows a country, even a high risk one, to borrow relatively easily in international financial markets.

Second, a period of prolonged deficits in the country’s current account balance and a large increase in foreign debt in foreign currency.

Third, an event that changes conditions or expectations in the international capital and financial markets. Such an event could be a global recession that reduces the demand for exports of the country that has accumulated high foreign debt, an increase in international interest rates, a political change in the country or a combination of these factors.

Fourth, a debt crisis is more likely to occur in countries with limited foreign exchange reserves that have adopted fixed exchange rate regimes or are participating in a monetary union.

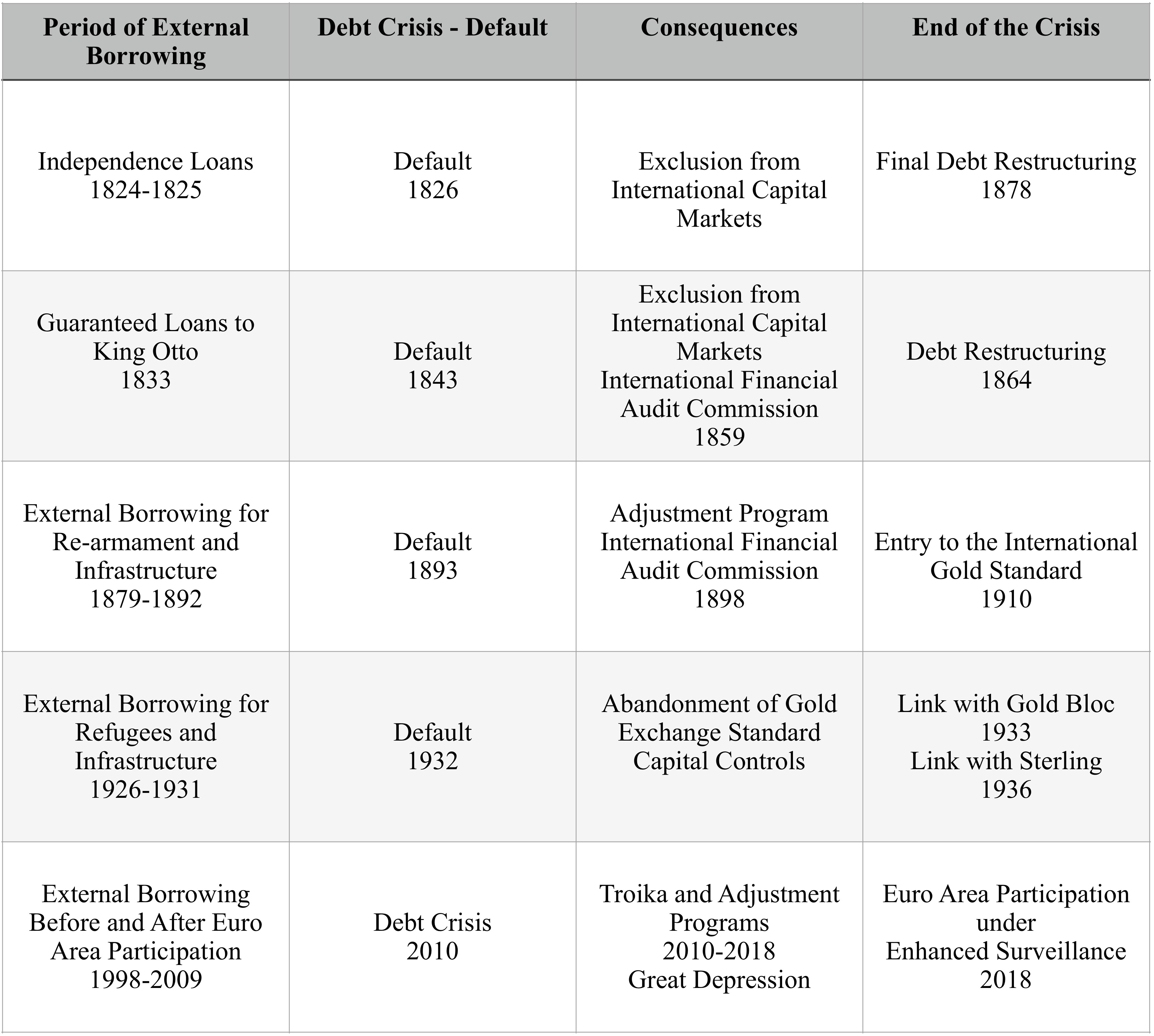

All four conditions applied in the case of the international debt crises and the defaults of Greece, which are briefly summarised in the Table below.

The defaults of 1826 and 1843 occurred because Greece was able to borrow internationally despite not meeting the financial conditions, as it did not have, nor was it expected to, have sufficient foreign exchange or gold inflows to service the loans. Moreover, the Loans of Independence, due to their extremely unfavorable conditions, would be impossible to service even if the economy of Greece was a normal economy and not an economy at war, without sufficient resources and state institutions.

On the other hand, the defaults of 1893 and 1932 and the debt crisis of 2010 were due to prolonged periods of high current account deficits and large increases in external debt. In the case of the defaults of 1893 and 1932 the external debt was denominated in foreign currency, while in the case of 2010, it was denominated in a currency which Greece could not issue or control. In all three cases, the trigger for the crisis came from international recessions that reduced demand for Greek exports of goods and services and changed international investors’ expectations regarding the country’s solvency.

In addition, the defaults of 1932 and the debt crisis of 2010 were associated with the country’s participation in a relatively rigid fixed exchange rate monetary regime (in 1932) or a single currency (in 2010).

The first stage of a debt crisis leads to a large reduction or cessation of international lending to the country, an increase in interest rates or, worse, an outflow of capital abroad. These tend to lead an economy into recession, as it has to reduce its current account deficit by reducing domestic investment and increasing national savings. A crisis often leads to a rapid devaluation of the currency, inflation, and even the collapse of the banking system, especially if the banks have also borrowed in foreign currency. Often, after a debt crisis, a country is forced to resort to official lending through a program that requires an adjustment program that usually includes currency devaluation, fiscal adjustment and monetary stabilization in order to bring the current account back into balance.

From the IFAC in 1843 to the Troika in 2010

All of the above have happened in the periodic debt crises that have affected the Greek economy. The default of 1843 was followed by the naval blockade of Piraeus and the imposition of an International Financial Audit Commission (IFAC), which oversaw the gradual repayment of Greece’s restructured external debt. The default of 1893 was followed by the imposition of an even stricter supervision through an even more empowered International Financial Audit Commission (IFAC). In exchange for a new official loan to repay its old debts, the IFAC imposed a strict fiscal and monetary adjustment that, at least initially, resulted in a major economic downturn. The default of 1932 was accompanied by devaluation, fiscal adjustment, prolongation of the recession and imposition of controls on capital movements. The 2010 debt crisis was accompanied by formal borrowing to refinance external debt and the imposition of three successive adjustment programs, designed and overseen by a “troika” of representatives from the IMF, the European Commission and the ECB. Although it contributed to the significant correction of the external and fiscal imbalances that characterized the Greek economy, this policy caused a major economic depression, which lasted seven years, between 2010 and 2016.

Following the coronavirus crisis, Greece needs to undetake significant reforms in order to improve its growth performance, so as to permanently raise the level of prosperity of the Greeks to the average of the EU countries. These reforms should focus on increasing domestic savings and the productive and fiscal efficiency of the economy, so that, within the framework of monetary stability ensured by Greece’s participation in the euro area, a new period of sustainable growth can emerge, without the twin deficits and other macroeconomic imbalances of the last 200 years.

© George Alogoskoufis

_________________________

The author is Professor and Head of the Department of Economics at the Athens University of Economics and Business and a Research Associate of the Hellenic Observatory, London School of Economics. This article was first published in Greek in the newspaper To Vima, on December 25, 2021. It is based on Historical Cycles of the Greek Economy (from 1821 to the Present) (Gutenberg Publications, 2021, in Greek), a new book by Professor George Alogoskoufis. It is also based on ongoing research reported in, Historical Cycles of the Economy of Modern Greece: From 1821 to the Present,Working Paper no. 1-2021, Department of Economics, Athens University of Economics and Business. and, GreeSE Paper no. 158, Hellenic Observatory, London School of Economics.