Growing worries about the return of a long-forgotten bugbear highlight increasing risks for savers

Martin Wolf, The Financial Times, March 26, 2021

A spectre is haunting investors: the return of inflation. But is it a plausible threat? And what would it mean if it did return?

These are almost certainly the most important economic questions investors confront. Unexpectedly high inflation would raise interest rates, destabilise exchange rates, ignite unrest in labour markets, push the highly indebted towards default and destabilise asset markets.

At present, significantly higher inflation seems a remote risk. But, after four decades of well-controlled inflation, the monetary and fiscal policies unleashed by the pandemic, as well as longer-term structural changes in the world economy, might ruin this comfortable perspective.

If we are to work out what this possibility might mean, we need to start by journeying into history.

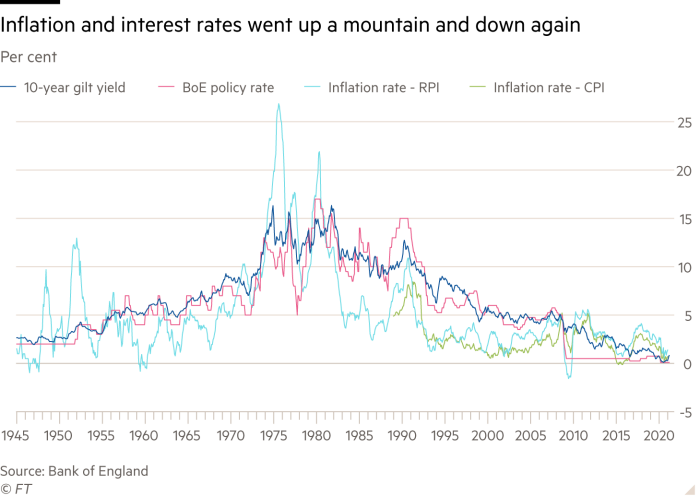

The last time inflation exploded out of control in high-income countries was the 1970s. The UK was very much in the forefront in this story. In August 1975, year-on-year retail price inflation reached 27 per cent. In April 1980 it spiked, once again, to 22 per cent (see charts).

The two oil shocks were important causes of soaring inflation. Yet there was a crucial domestic side to the narrative. A vicious spiral of high inflation, wage controls and labour militancy characterised the decade. In January 1974, in response to a strike by coalminers, Edward Heath, the prime minister, even declared a three-day week.

The UK appeared to be on the verge of turning into Argentina, a country notorious for worker militancy and high inflation. But it was not alone. Italy’s inflation experience was as bad as that of the UK. Other high-income countries suffered too.

Among today’s Group of Seven leading high-income countries, Germany did much the best: its average rate of consumer price inflation in the 1970s was below 5 per cent, against the UK’s 13 per cent, while that of the US was 7 per cent. Germany’s relative success helped strengthen the case for an independent central bank and a counter-inflationary anchor for monetary policy.

The 1970s were an era of stagflation — high inflation and low growth. They were also, as a result, an era of terrible performance for asset prices.

For the holders of bonds, mostly older people who relied on them for security in old age, a decade of high inflation was a financial disaster. Stocks did terribly, too. The cyclically-adjusted price/earnings ratio (CAPE), developed by Nobel laureate Robert Shiller, collapsed from 24 in 1966, to 8 in 1974 and 7 in 1982.

US market valuations nearly fell back to levels seen in the Great Depression years of the early 1930s. The ratio of the value of the stock market to UK gross domestic product fell to a low of 11 per cent in 1974. In the US, the trough was 21 per cent in 1982.

At these valuations, the stock markets were saying that capitalism was finished. What had caused this disaster?

First, came the inflationary fiscal and monetary policies of the late 1960s and early 1970s, the surge in the price of oil, labour unrest, failed controls over wages, price controls, and squeeze on profits, made worse by the failure to adjust taxation for the impact of inflation. Later, came the tight monetary policies of the early 1980s of Paul Volcker, chair of the Federal Reserve, in the US and Margaret Thatcher and her chancellor Geoffrey Howe, in the UK.

After these painful years, control over inflation moved to centre stage. The notion that inflation was a price worth paying for lower unemployment was rejected as a failed theory. Initially, the alternative was the monetary targeting recommended by Milton Friedman.

When this turned out not to work as well as hoped, policymakers shifted from the targeting of an instrument, money, to the targeting of the goal, inflation. Formal targeting of inflation began in New Zealand in the early 1990s and spread, along with central bank independence, to much of the world, notably including the UK.

The successful control of inflation coincided with the beginning of a prolonged and remarkable boom in asset prices.

The extended bull market in bonds was an automatic consequence of rapidly declining inflation. That was further strengthened by a collapse in real interest rates to today’s negative levels. It was not hard for a manager of bond funds to seem a genius.

Much the same was true for equity fund managers. In the US, the CAPE rose to 44 in 2000, an all-time high. The only bull market that came close to this one was that of the 1920s. The ratio of the value of the stock market to GDP soared to 162 per cent in the UK and 157 per cent in the US in 2000. Capitalism was triumphant.

The peak of 2000 in the “dotcom bubble” was followed by a crash and then yet another one after the financial crisis of 2007-08. Nevertheless, the US market recovered: at the end of 2020, the US CAPE was the second highest on record and the stock market was worth 187 per cent of US GDP.

The move to free-market economics

The success in controlling inflation was far from the only force driving this great bull market. It was part of a broader swing away from the regulated post-second world war economy towards free-market economics: the weakening of trade unions; tax cuts; trade liberalisation; financial deregulation; and the opening up of capital flows.

In a classic analysis, published in 2004, Harvard University’s Kenneth Rogoff argued that this increase in competitive pressure, some of it coming from China’s entry into the world economy, was a key factor behind the success of the disinflationary policy.

One might add that these changes — disinflation, deregulation and globalisation — also led to a fundamental swing in economic and political power, away from labour and towards the owners of capital. This, too, promoted the bull market.

An important question is why the inflation-disinflation cycle — indeed, so much of what has happened economically — was so similar across high-income countries. The answer must be that they are both exposed to shared ideas and connected through commerce, capital flows and monetary policy.

Another salient characteristic of the past four decades has been expanding debt, initially mainly private debt, driven by financial deregulation. After the global financial crisis in 2007 and 2008 and the eurozone crisis that followed, government debt also soared.

The debt accumulation has also been the consequence of structurally weak demand across the world economy. In 2005, former Federal Reserve chair, Ben Bernanke, called this phenomenon “the savings glut”. More recently, former US treasury secretary, Lawrence Summers has termed it “secular stagnation”.

The result of this has been falling and ultimately negative real interest rates and, given the low inflation rates, as well, near-zero or even negative nominal interest rates, especially in times of severe crisis.

The Asian financial crisis of 1997-98 and the bursting of the dotcom bubble in 2000 were just intimations of what might happen. The big shock to the system was the global financial crisis, which was met by a huge monetary and fiscal response.

Some worried then that this would end the era of low inflation. That fear turned out to be misplaced. Premature fiscal tightening and a weak monetary policy response, especially in the eurozone, led, instead, to a disappointing recovery and persistently sub-target inflation in the US and eurozone.

The lesson learned from this disappointing experience was that the response must be quicker, bigger and more determined next time. Covid-19, a quite different kind of shock, turned out to be that “next time”. It was met by extraordinary fiscal and monetary action, to stabilise the economy and people’s incomes.

Is this second huge shock in 12 years going to trigger what the global financial crisis did not — the shift towards high inflation, which many on the right then feared, and the revolt against capitalism, which many on the left then desired?

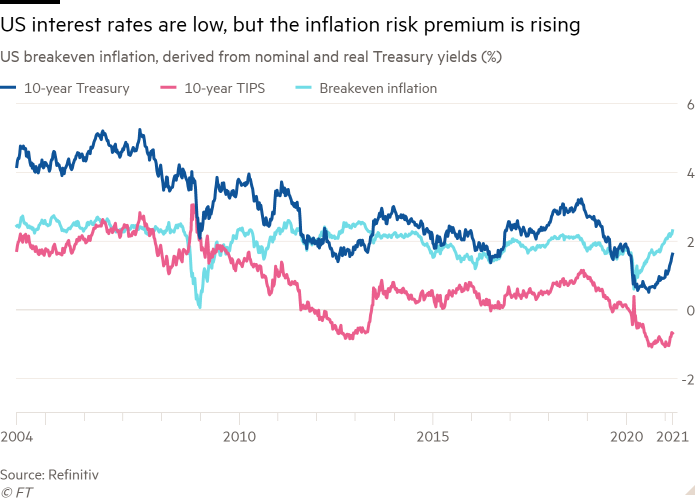

This is certainly not what markets now expect. They expect a healthy recovery. Bond markets merely indicate a modest and desirable rise in inflation expectations and inflation-risk premiums, especially in the US. Stock markets also remain confident of future profitability.

The dominant concern of central banks, notably the Federal Reserve, is still to raise inflation, not keep it down. Central banks hope that, with higher inflation and inflation expectations, they would be able to raise interest rates well above zero. This would give them more room for manoeuvre in future, in response to negative shocks.

Furthermore, central banks believe that, in today’s economy, the response of wages to unemployment is very weak. This means they are able to run economies “hot”, with little fear of an unduly strong rise in inflation.

Politics has changed, too, especially in the US, with the election of Joe Biden as president. The ideas of “Modern Monetary Theory” — the view that the only constraint on monetary financing of government is inflation, which, in turn, is best controlled by fiscal policy — has won much intellectual favour on the left. So, too, has the conviction that there must be a rebalancing of the relationship between labour and capital, in favour of workers.

These new perspectives have now come to fruition with the passage in the US of a $1.9tn fiscal stimulus programme supported by an expansionary monetary policy expected to last at least until 2024, even though the Fed forecasts US GDP growth as high as 6.5 per cent this year. The administration is also thinking of a further $3tn in spending on longer-term priorities, including the green economy. In total, these programmes would amount to almost a quarter of US GDP. That is transformative policymaking.

Summers has criticised the approach, telling Bloomberg: “These are the least responsible fiscal macroeconomic policy we’ve have had for the last 40 years.” Furthermore, “it’s fundamentally driven by intransigence on the Democratic left and intransigence and the completely irresponsible behaviour in the whole of the Republican Party”.

The likelihood, then, is that there is going to be a huge expansion in spending and little in the way of additional taxation. Given the monetary expansions, too, the chances of an inflationary overshoot have substantially increased.

If this happens in the US, worldwide spillovers are quite likely, not least in the UK. But in other high-income countries, too, household savings are high, fiscal deficits large and monetary policy expansionary. The kindling needed to light an inflationary fire can be seen almost everywhere.

Distorting the economy

In the 1970s, the British economist, Charles Goodhart, propounded what came to be called Goodhart’s law: “Any observed statistical regularity will tend to collapse once pressure is placed upon it for control purposes.” This “law” could help explain the failure of monetarism.

This law may have a corollary: “A statistical relationship, once ignored, will become relevant.” If so, the Phillips curve, which links unemployment and inflation, or the relationship between broad money and spending might come back to bite us.

So what would it mean for investors if inflation were to rise well beyond 2 or 3 per cent? The initial effect would be to increase profits and so be good for equities, but the inflation would be terrible for bond markets.

High inflation tends to distort the economy, partly because taxes are imperfectly adjusted for inflation. It will raise long-term interest rates. That will undermine the solvency of many debtors, including corporate debtors, as debt is rolled over.

Above all, an inflationary overshoot will trigger a disinflationary response from central banks. That will mean much higher policy rates. That could lead to waves of default far more pervasive than in the early 1980s, when the big story was the debt crisis in developing countries. This time, the debt crises could be almost everywhere, because there is so much more debt.

These risks could also interact with the structural threats laid out by Goodhart and Manoj Pradhan in The Great Demographic Reversal. The economic regime that began in the 1980s is, they argue, coming to an end, with rising protectionism and rapid ageing in all the important economies, including China.

As labour forces shrink, this book suggests, the number of consumers will rise relative to the number of producers, thereby raising prices. Fiscal pressure will rise inexorably, as the population ages. If governments have to choose between inflation and fiscal tightening, they will choose the former. Finally, if interest rates rise too high for comfort, governments will force central banks to lower them.

Ultimately, then, these pressures would end in another era of high inflation. Some will note, against this view, that this is not how things have ended up in Japan, where decades of easy money has failed to ignite inflation.

Maybe, that will now happen in the world as a whole: we will all end up Japanese. Certainly, history never repeats exactly.

The stagflation of the 1970s, especially the squeeze on profits and stock market collapse, were due to features of the economies of that time, especially the political strength of labour. So, things may play out quite differently this time.

Inflation has not come back. It may never do so. But the political and policy shifts we are seeing today, after Covid, together with the longer-term changes in the world economy, have raised the chances of an inflationary shock of some kind. Investors must take this possibility into account.